Ocean carriers face navigating seas of red ink in the wake of a Red Sea security crisis resolution

Supply-demand imbalance anxiety increasing as slowdowns in North American imports and global economic growth point to international trade deceleration in 2026

Global trade lane disruption deceleration could accelerate ocean carriers’ bottom-line profit erosion.

That counter-intuitive math was discussed during the December 4 Journal of Commerce/S&P Global Market Intelligence World Shipping Outlook 2026 webcast.

Moderated by Journal of Commerce executive editor Mark Szakonyi, the outlook panel predicted a bad moon rising for ocean container carriers in 2026.

Key factors in that forecast: ballooning containership capacity and shrinking consumer demand.

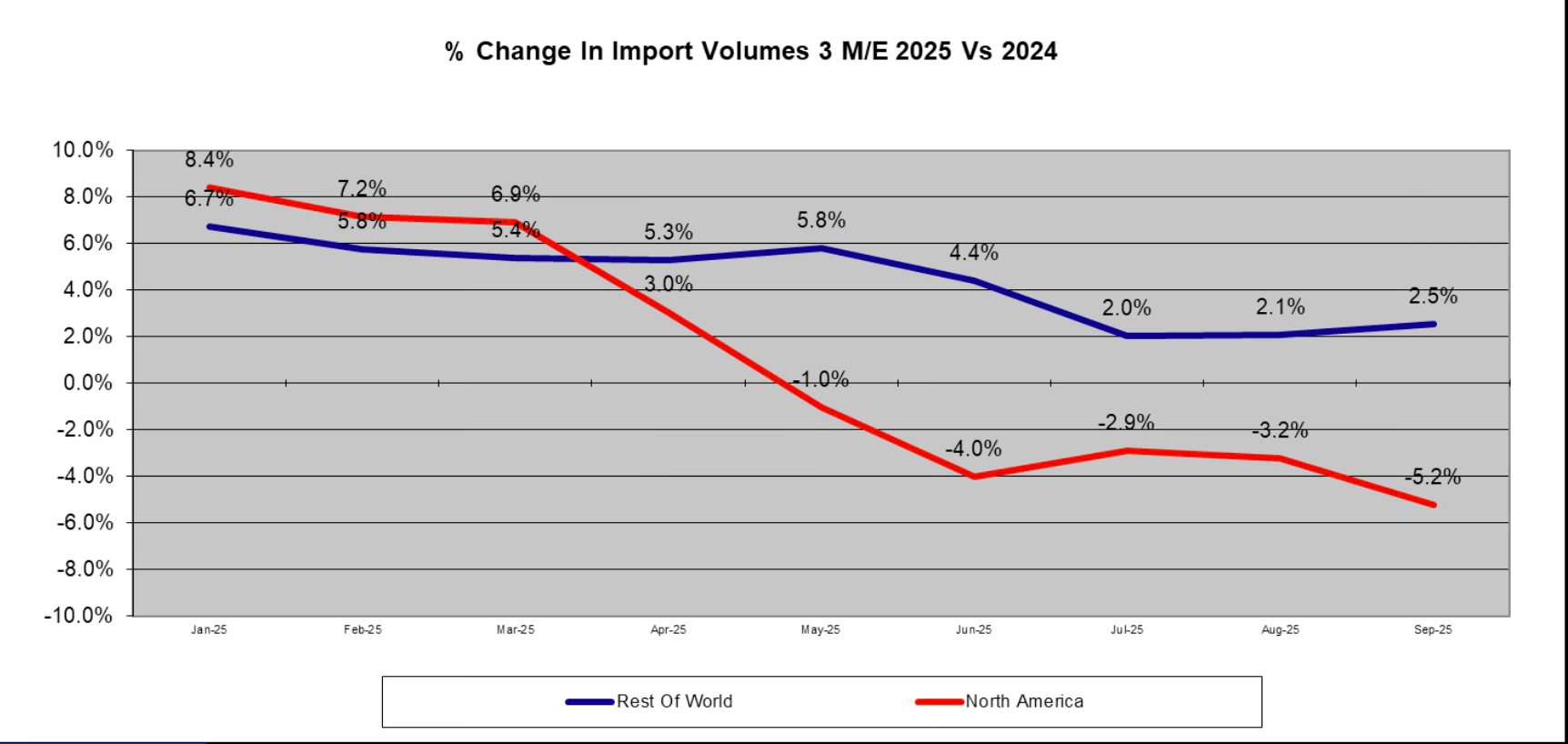

As New York-based container shipping analyst John McCown outlined in his presentation, North America’s container cargo flow has been slowing for most of 2025.

October volume, he said, “came in about 8% less than [the same month] last year. In a way, that’s really the first consistent tariff-related reduction. It’s going to be worse in November and December.”

McCown added that the gap between cargo flowing into North America and into the rest of the world is widening.

According to his data, North America’s container imports during the latest three-month period for which data is available were down 5.2% compared with a 2.5% increase in the rest of the world.

“What’s happened,” McCown said, “is supply chains [have] mitigated the clear weakness in U.S. volume by [moving] higher imports elsewhere.”

The cargo shift has thus far not torpedoed ocean-carrier bottom lines.

McCown’s overview of the industry’s dramatic pre-pandemic to post-pandemic earnings reversal is a multibillion-dollar 21st-century rags-to-riches tale.

When the pandemic shut down global trade and then triggered a sudden spike in consumer goods demand – especially in North America – container shipping boomed, as did supply chain chaos, port congestion and ocean carrier profits.

Shipping line financials shot up from a cumulative US$8.5 billion loss in the four-year lead-up to the pandemic to what McCown has previously noted was a five-year string of positive earnings-to-revenue margins ranging from 8.1% in 2020 to 46.1% in Q2 2022.

The earnings inflow bonanza lost momentum in 2023 but rebounded in 2024. Houthi terrorist attacks on Red Sea shipping that have diverted commercial vessels away from the Suez Canal generated much of that good financial fortune.

Longer voyages around the Cape of Good Hope have effectively reduced container shipping capacity by an estimated 8%. That reduction has offset what would have been a container shipping oversupply.

As McCown noted: “Disruption has been extraordinarily good to carrier financial results.”

“I think that the industry is going to suffer badly through 2026.”

– John McCauley, shipping consultant and former Cargill executive

However, a Red Sea security crisis resolution would release that fleet capacity back into the market. Add that to all the new containerships set to join the world’s fleet, and you have oversupply, freight rate deflation and port congestion, especially in Europe.

So, it’s no surprise that container shipping lines remain Suez-averse.

Asked during a recent Hapag-Lloyd (ETR:HLAG) market update if the company had any near-term plans to return to the Suez, the company’s CEO Rolf Habben Jansen said, “No. Not at this time.”

He added that Hapag-Lloyd, the world’s fifth-largest container shipping line and a member of the Gemini Cooperation alliance with Maersk (CPH:MAERSK-B), would need to be assured of a “safe and sustainable” Red Sea before it contemplated any return to the Suez.

“We are now a little bit over two years into this crisis … [and] we have seen close to 100 attacks on ships … [and] we’ve had periods before that it looked quiet, and then we returned to where we were before. … We have a plan on the shelf on how to return, but … returning to Suez will be difficult.”

And, again, any widespread Red Sea shipping revival would release a lot of containership capacity into a depressed market.

Ines Nastali, S&P Global senior supply chain analyst, pointed out that in 2025’s first half, 134% more containerships were ordered than in the same period in 2024.

That ocean carrier newbuild exuberance is not unique to 2025.

Nastali said container liners ordered 309% more ships over 2024’s latter half compared with 2023’s last six months.

Trade data from other sources also points to container shipping market challenges ahead.

December’s UNCTAD 2025 Trade and Development report estimates that global growth will slow to 2.6% in 2025, which is down from 2024’s 2.9%, and continue at a 2.6% pace into 2026.

It forecasts that U.S. economic growth will slow to 1.8% in 2025 and slip further to 1.5% in 2026. The report also has Canada’s GDP growing at a meagre 1.1% this year and 1% in 2026.

Economic recovery in Carney Canada is expected to be next to non-existent in 2026, or as UNCTAD diplomatically puts it: “economic activity is expected to recover, albeit at a very modest pace.”

U.K. shipping industry consultancy Drewry provided more trade deceleration data recently.

As of November 28, its Drewry Container Equity Index (DCEI), which tracks publicly traded container shipping company stock performance, was up 1.1% week over week (WoW), an increase that underperformed the S&P 500’s 3.7% increase during the same period.

Year to date, the DCEI is down 0.6%. That compares with the S&P 500’s 16.4% increase.

So, what are 2026’s freight rate recovery odds?

Not good.

As shipping consultant and former Cargill executive John McCauley said during the JoC webcast, “I think that the industry is going to suffer badly through 2026. I think rates are going to go lower. And I think we’re going to see very poor results for the carriers, and I think they’re going to find their customers are really struggling.”

www.linkedin.com/in/timothyrenshaw

@trenshaw24.bsky.social

@timothyrenshaw